AEMO’s latest analysis of Quarterly Energy Dynamics (QED) report showcases recent insights into the transformation underway across Australia’s energy systems and markets.

As observed in AEMO’s control rooms, renewable generation continues to grow, setting minimum operational demand records and driving periods of zero or negative prices, while synchronous condensers improve system strength in South Australia and batteries provide the majority of Frequency Control Ancillary Service (FCAS) for the first time.

Changing generation portfolio

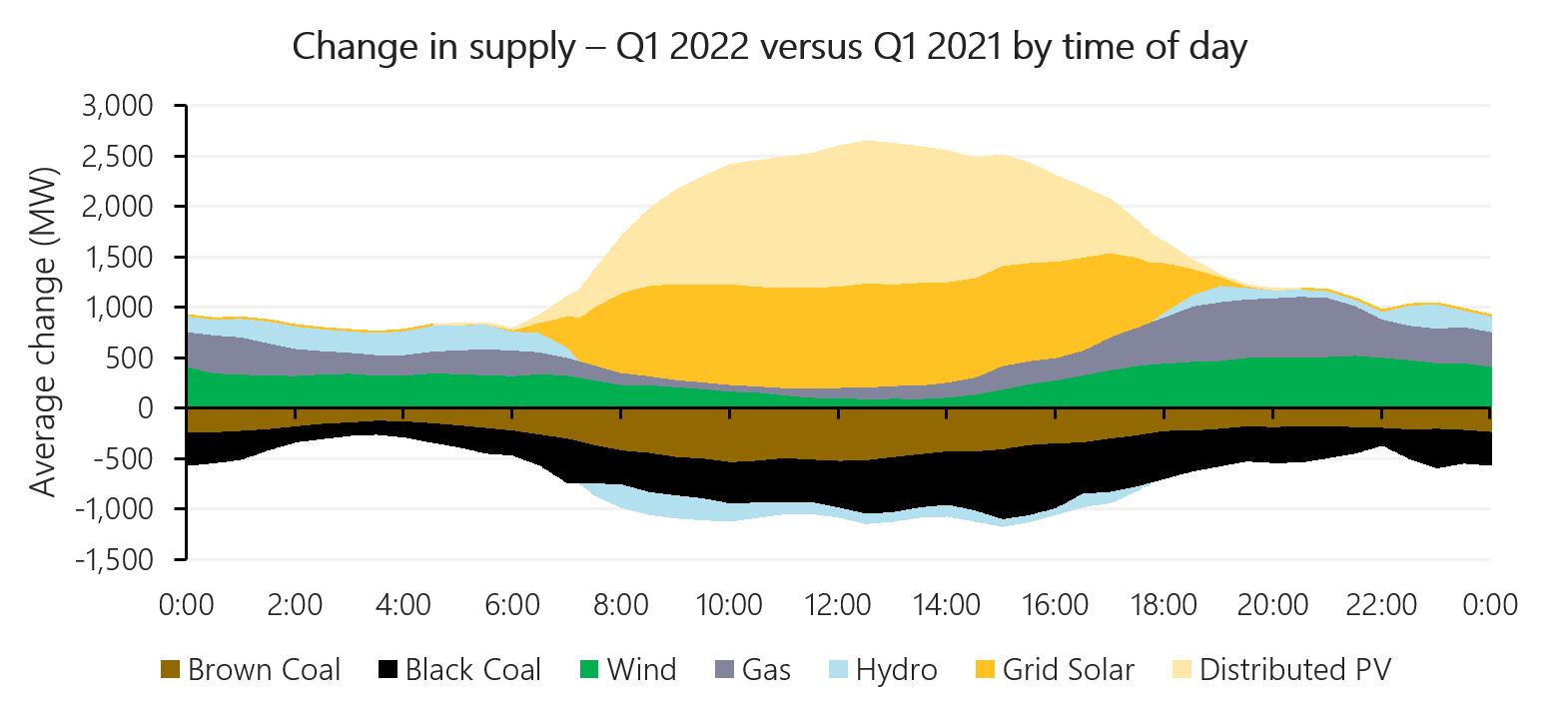

In the March 2022 quarter, increased output from grid-scale wind and solar generators (+743 megawatts) and distributed PV (+460 MW) helped renewable energy hit a market share of 33.7% in the National Electricity Market (NEM). Maximum instantaneous renewable penetration peaked at 61.3%, marginally below Q4 2021’s 61.8%

Conversely, coal-fired generation share fell to 60.4%, a drop of over 5 percentage points from Q1 2021, with declines seen in brown coal (304 MW) and also black coal generation (374 MW), which hit its lowest Q1 average in two decades.

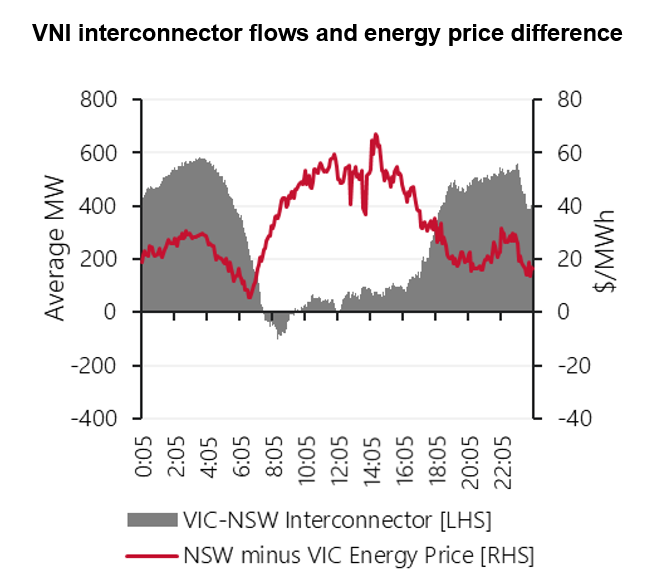

Transmission constraints limited cheaper energy sharing

Amplifying the trend noted in the December 2021 quarter, exports from southern NEM regions to higher-priced northern regions via the Victoria to New South Wales interconnector (VNI) during this quarter were more restricted by transmission constraints (to address system security risks).

The impact of key daytime transmission constraints is evident in reduced average export limits for VNI, profiled by time of day, in Q1 2022 relative to Q1 2021.

Average export limits fell by more than two thirds over morning hours (0800 hrs to 1200 hrs) and remained significantly lower until late evening.

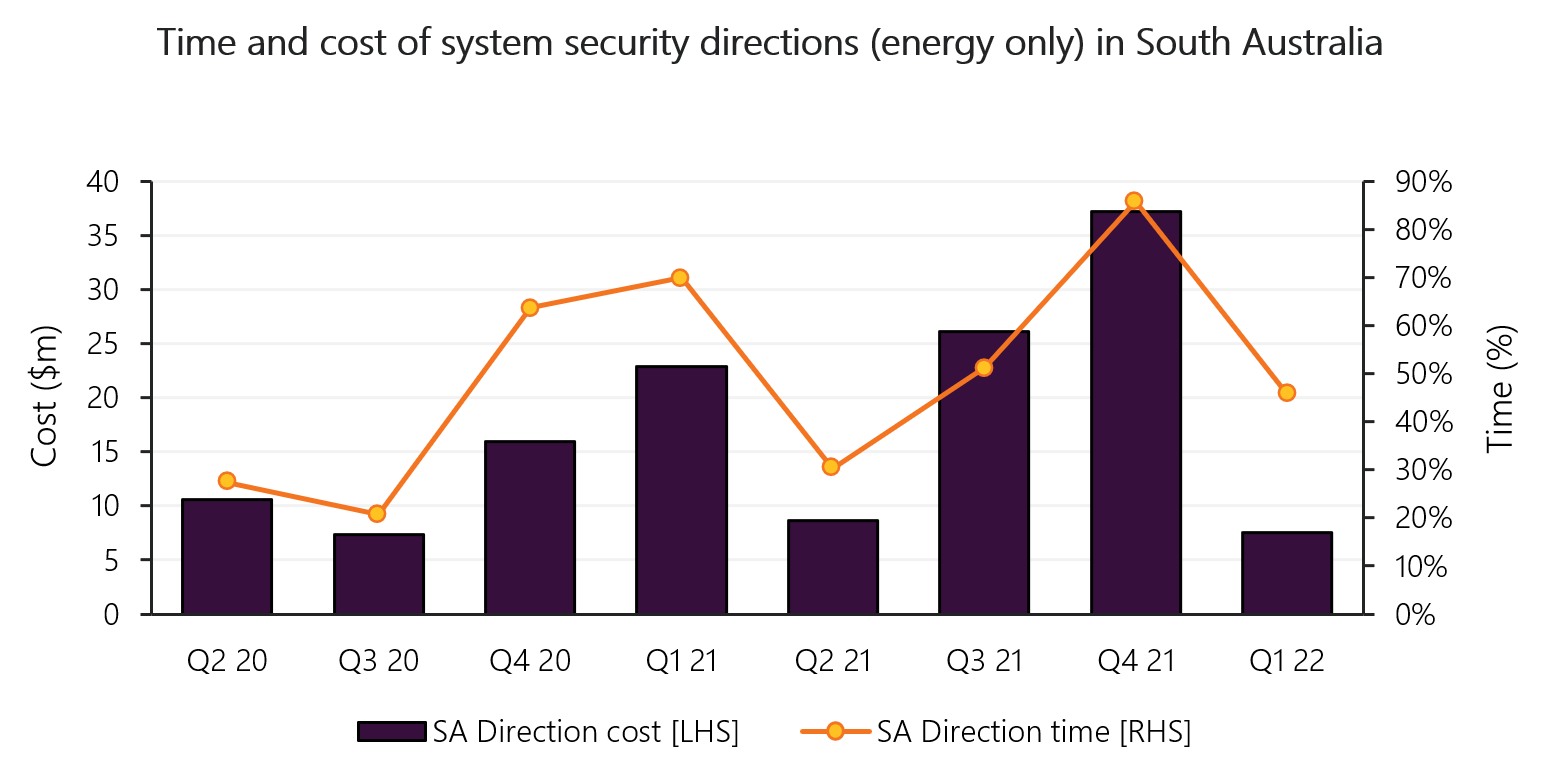

Synchronous condensers reduce directions costs, enable higher renewable output

In South Australia, the first quarter of full operation with four synchronous condensers saw the costs of system security directions to gas generators fall to $7.5 million in 2022 Q1, down from $37 million in Q4 2021 and $23 million one year ago.

This is attributable to full operation of four synchronous condensers allowing reduced minimum levels of online gas generation for the whole quarter, and higher local spot prices inducing gas generators to remain online for economic reasons.

The synchronous condensers were procured by South Australia’s transmission network operator, ElectraNet, to meet declared system strength and inertia shortfalls identified by AEMO.

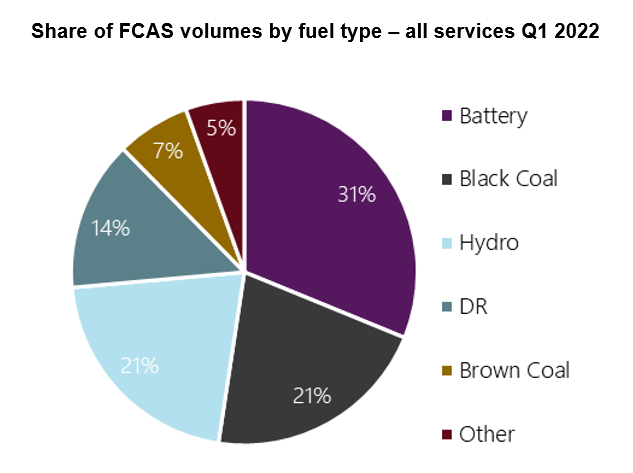

Batteries reach majority for FCAS

Grid-scale batteries were the largest providers by fuel/technology type of FCAS in Q1 2022, reaching a combined share of 31% across the NEM’s eight FCAS markets.

Other relatively new sources, including demand response and Virtual Power Plants (VPP), have also grown volumes at the expense of conventional generation providers.

Estimated battery revenues from energy market participation also increased to their highest quarterly level since Q1 2019.

AEMO’s latest Generation Information file shows that alongside 487 MW of utility-scale solar and 210 MW of wind capacity moving to the committed phase, there are 26,790 MW of proposed battery storage systems, a significant increase on the 611 MW of existing capacity in the NEM.

These and many other insights into Australia’s electricity and gas markets can be found in AEMO’s Quarterly Energy Dynamics reports, available on the AEMO website.